All Activity

- Past hour

-

Credit deflation and the reflation cycle to come (part 9)

Errol replied to spunko's topic in Property Prices & Economy

-

Credit deflation and the reflation cycle to come (part 9)

Funn3r replied to spunko's topic in Property Prices & Economy

After @spunko explained about Jersey potatoes being International Kidney I planted some and they seem to be doing alright. -

Property crash, just maybe it really is different this time (Part 3)

With a crooked smile replied to spunko's topic in Property Prices & Economy

Obviously buy to let landlords to house the new British. -

Credit deflation and the reflation cycle to come (part 9)

Funn3r replied to spunko's topic in Property Prices & Economy

That's me. I try similar from time to time. for example my mythical George Floyd sandwich grill. I do find it funny how many people cannot spell "rogue state" so it somehow ends up as rouge. -

Credit deflation and the reflation cycle to come (part 9)

Lightly Toasted replied to spunko's topic in Property Prices & Economy

Very interesting. The status of reserve currencies is called "exorbitant privilege"; I always wondered "exorbitant for whom?" In the long term it's exorbitant to the issuer, of course, though that's not what's meant. -

Credit deflation and the reflation cycle to come (part 9)

Long time lurking replied to spunko's topic in Property Prices & Economy

Nothing to see here mover along it`s just market sentiment -

The UK's Q4 2023 banking crisis.

sancho panza replied to sancho panza's topic in Property Prices & Economy

this is an interesting article which blames poor share price perfrmance for UK banks on UK govt-of course-,UK economy,regulatory issues-needing solid capital ratios (heaven forbid),markets not seeing the value(Bailey's theory) 'Barclays actually trades at a 50pc discount to the book value of its assets.' the otehr thesis might be that actually the marekts are valuing them jsut right and that their loan books are hiding losses through forebearance and an over reliance on easy moentary policy. https://uk.yahoo.com/news/british-banking-become-stagnant-backwater-093000644.html British banking has become a stagnant backwater – and it’s painfully obvious why Deals are suddenly back in vogue and “consolidation” is the word on everyone’s lips. Nationwide Building Society is paying £2.9bn to buy Virgin Money – thereby increasing in size by about a third. Coventry, the second biggest building society in the country, is planning to buy the Co-op from its hedge fund owners for £780m. Excuse me while I stifle a yawn. A bit of M&A action will no doubt make a welcome change for those advisers whose thumbs must have become over-muscled from so much twiddling. But anyone tempted to suggest these deals indicate animal spirits are returning to the City is barking up the wrong tree. In reality, this all, like the recent something-and-nothing strategy overhaul from Barclays, amounts to so much displacement activity. It highlights the extent to which the industry is bogged down, devoid of fresh thinking and stymied by negative investor perceptions of the UK economy. The defining characteristic of UK banks is that they are massively undervalued compared to their international peers, a fact that Andrew Bailey pointed out in a speech in February and which he described as “puzzling”. The Governor’s intervention came soon after Jeremy Hunt had called bank chiefs into No 11 for a chat about why their share prices were doing so badly. Oh, to have been a fly on the wall at that meeting. If the bankers were being honest, their list of reasons would surely have included the Governor of the Bank of England and the Chancellor of the Exchequer. To understand why, we need a little context. The share prices of UK banks fell off a cliff in April 2007 and have basically just bumped along the seafloor ever since. This is sometimes blamed on enduring memories of the financial crisis and regulatory demands to hold more capital. But both these factors are just as true of international banks as they are of British ones. The bulk of bank regulations are set globally. Watchdogs around the world are currently in the process of implementing the last leg of the post-financial crisis capital reforms known as Basel 3.1. Sure, it’s taken a while, but the new regime can broadly be considered a success given the ease with which most big banks navigated the economic turbulence of the last four years. Never the less, something is amiss in the UK. As Bailey pointed out in his February speech, the average price to tangible book ratio for the major UK banks in the two years before Northern Rock imploded in 2007 was 3.4. That figure is now 0.7. In other words, the market believes UK lenders are worth less than the sum of their parts. Barclays actually trades at a 50pc discount to the book value of its assets. This is one of the worst valuations of a large bank in the Western world. NatWest, Lloyds and HSBC are faring a little better but not much. Normally such deep discounts would suggest investors are worried there are nasties lurking on balance sheets. That’s not the case here. “The paradox is starkly apparent – a period when banks were valued by markets at more than 300pc of tangible book value ended in disaster,” said Bailey. “Today’s greater stability looks the better place to be, but not for market valuations. That leaves us with the puzzle.” Yeah, I’m not sure it’s that much of a head-scratcher. When all is said and done, investors who take a stake in a bank are really placing a bet on the economy or economies in which those lenders operate. Shareholders in UK banks have been hit with additional levies on top of normal corporate taxation since 2011 and the Bank of England’s decision to ban lenders from paying dividends during the pandemic. Add to that the political chaos of recent years – culminating in Liz Truss’s cluster-Budget – together with the lack of any credible plan to stimulate strong economic growth since, and it becomes clear that the main issue with UK banks is not the “banks” bit but rather the “UK” part. Of course, HSBC, which generates two-thirds of its profits in Asia, is a partial exception, although exposure to China is clearly a mixed blessing at the moment. Many analysts believe that the latest Barclays rejig will result in the bank becoming even more focused on the UK. Yay! And the real problem with their low valuations is that it isn’t much of a problem. Many bargain-basement UK companies are currently being snapped up by foreign buyers, but there’s no way regulators will allow that to happen to banks. Nor will they let the big four acquire each other, as this would reduce competition yet further. Meanwhile, the sheer volume of post-crisis rules, although necessary, has made the regulatory moat around the bigger firms even wider and deeper. Despite being the largest challenger bank in the UK, Virgin Money’s cost of equity was in the low teens, while its return on equity struggled to escape single digits, meaning it was burning through shareholder value. No wonder its owners are tapping out. The UK banking industry has come to resemble a stagnant pond. Now and then a sprat will swallow a minnow; flashy fintechs might create a bit of a buzz. But the ecosystem is low on the oxygen of real competition. UK banks are safer now. However, they are medium-sized fish sluggishly drifting through a shrinking backwater. - Today

-

Credit deflation and the reflation cycle to come (part 9)

Axeman123 replied to spunko's topic in Property Prices & Economy

Yahoo finance with an epic opening paragraph: Mortgage lenders hike interest rates as market jitters set in https://uk.finance.yahoo.com/news/mortgage-interest-rates-latest-barclays-hsbc-natwest-halifax-151133798.html Meanwhile Sunak confirms ESG just means "aligned with government policy priorities" PM says investments in weapons companies meet ethical criteria https://uk.finance.yahoo.com/news/pm-says-investments-weapons-companies-153120348.html -

Credit deflation and the reflation cycle to come (part 9)

Long time lurking replied to spunko's topic in Property Prices & Economy

Well on the plus side it`s by 2030 so likely never to happen -

Credit deflation and the reflation cycle to come (part 9)

Axeman123 replied to spunko's topic in Property Prices & Economy

Indeed, that is likely what the final delay on rate cuts will be - waiting for markets to drop yields on their own first. IIRC the big Fed hikes came when market yields started running ahead of them. -

Credit deflation and the reflation cycle to come (part 9)

belfastchild replied to spunko's topic in Property Prices & Economy

I went out and counted my potato stash. Which reminds me to get the next ones into the ground soon. -

Credit deflation and the reflation cycle to come (part 9)

Long time lurking replied to spunko's topic in Property Prices & Economy

Just like commodities the price today reflects the price you will pay months /years down the line rather than today The shit really hits the fan when bonds exceed the Fed`s base rate though at this point everything sold prior to that point gets a hair cut -

Credit deflation and the reflation cycle to come (part 9)

Axeman123 replied to spunko's topic in Property Prices & Economy

I do know it was pied a terre btw, the frogs call potatos "apples of the ground" for some reason if directly translated. I was expecting laugh reactions, so now I wonder: Did no one else spot it? Did they spot it and feel bad for me pointing it out because they thought I didn't know? Was everyone just too cool to ruin the incredibly subtle joke? -

Credit deflation and the reflation cycle to come (part 9)

janch replied to spunko's topic in Property Prices & Economy

Housing in US: https://www.zerohedge.com/markets/bidens-america-40-renters-think-theyll-never-own-home-27-last-year What a sad state of affairs. Meanwhile in the UK Bristol is the van-dwelling capital: https://www.bbc.co.uk/news/uk-england-bristol-68597681 Look at them lined up on the Clifton Downs -

Credit deflation and the reflation cycle to come (part 9)

Bobthebuilder replied to spunko's topic in Property Prices & Economy

Apple. Sorry didn't read the quote correctly. Potato. -

Credit deflation and the reflation cycle to come (part 9)

janch replied to spunko's topic in Property Prices & Economy

Sorry I just had to comment................it caused me some merriment......I don't think they're after potatoes...... -

Credit deflation and the reflation cycle to come (part 9)

Loki replied to spunko's topic in Property Prices & Economy

US rate is already 5.25% - 5.50% though? -

Credit deflation and the reflation cycle to come (part 9)

Long time lurking replied to spunko's topic in Property Prices & Economy

-

Credit deflation and the reflation cycle to come (part 9)

DoINeedOne replied to spunko's topic in Property Prices & Economy

I know a few people working their asses off just to pay bills as she said its not living I

-

Credit deflation and the reflation cycle to come (part 9)

Axeman123 replied to spunko's topic in Property Prices & Economy

Stopped reading at that point tbh. -

Credit deflation and the reflation cycle to come (part 9)

DurhamBorn replied to spunko's topic in Property Prices & Economy

On the metals,this short term knock back is just what we want to see,violent weak hands shaken out.I expect the next leg up will be even more violent.Market is selling because it sees 5% rates BUT if/when inflation turns up again real rates will be -2%+ rocket fuel to metals and will see a huge transfer of wealth from bonds/bubble stocks etc to real assets. -

Credit deflation and the reflation cycle to come (part 9)

sancho panza replied to spunko's topic in Property Prices & Economy

this is one of those one of tax victoreis that will be a fleeeting victory as more people with moeny will leave.utterly derpessing to be facing death and knowing the WEF acolytes in westmisnter will be blowing 40% or so of your savings on bennies for people who have likely never saved very hsort sighted but that seems to be the plan these days with things like the windfall tax on north sea-one great photo op for the MSM then expensive/cold winters for the population also some interesting detail on QE losses of £45bn for BoE.which Im not seeing leading the 6 o clock news whihc it should. https://www.telegraph.co.uk/business/2024/04/23/inheritance-tax-hits-record-stealth-raid-hunt/ Inheritance tax take hits record £7.5bn after stealth raid by Hunt Data published by HM Revenue & Customs showed it received £7.5bn in inheritance tax (IHT) receipts in the financial year to the end of March, £400m above the same period last year. The amount raised from IHT has surged in the past few years after the Chancellor froze the threshold at which it is payable at £325,000 until 2028, preventing it from rising in line with inflation and forcing more families to pay. The deficit stood at £11.9bn last month, according to figures published by the Office for National Statistics (ONS). This is higher than the £10bn predicted by economists and means the Government borrowed £120.7bn to plug the gap between tax receipts and public spending in the 2023-24 financial year. It is also £6.6bn above the borrowing target set just a month ago by the Office for Budget Responsibility (OBR), the Government’s tax and spending watchdog. The figures also show the Government transferred almost £45bn to the Bank of England last year to cover losses on its bond buying programme. The Bank hoovered up around £900bn in debt during the financial crisis and pandemic, turning a profit as the returns on the gilts it bought outstripped the interest it paid to commercial banks on reserves. However, this has turned into losses as the Bank has raised interest rates to 5.25pc in the wake of Russia’s invasion of Ukraine. The Bank is also selling some of its bonds at steep losses as it actively winds down its balance sheet. The Bank currently estimates total net losses of £80bn to the taxpayer over the next decade. -

Credit deflation and the reflation cycle to come (part 9)

JREWING replied to spunko's topic in Property Prices & Economy

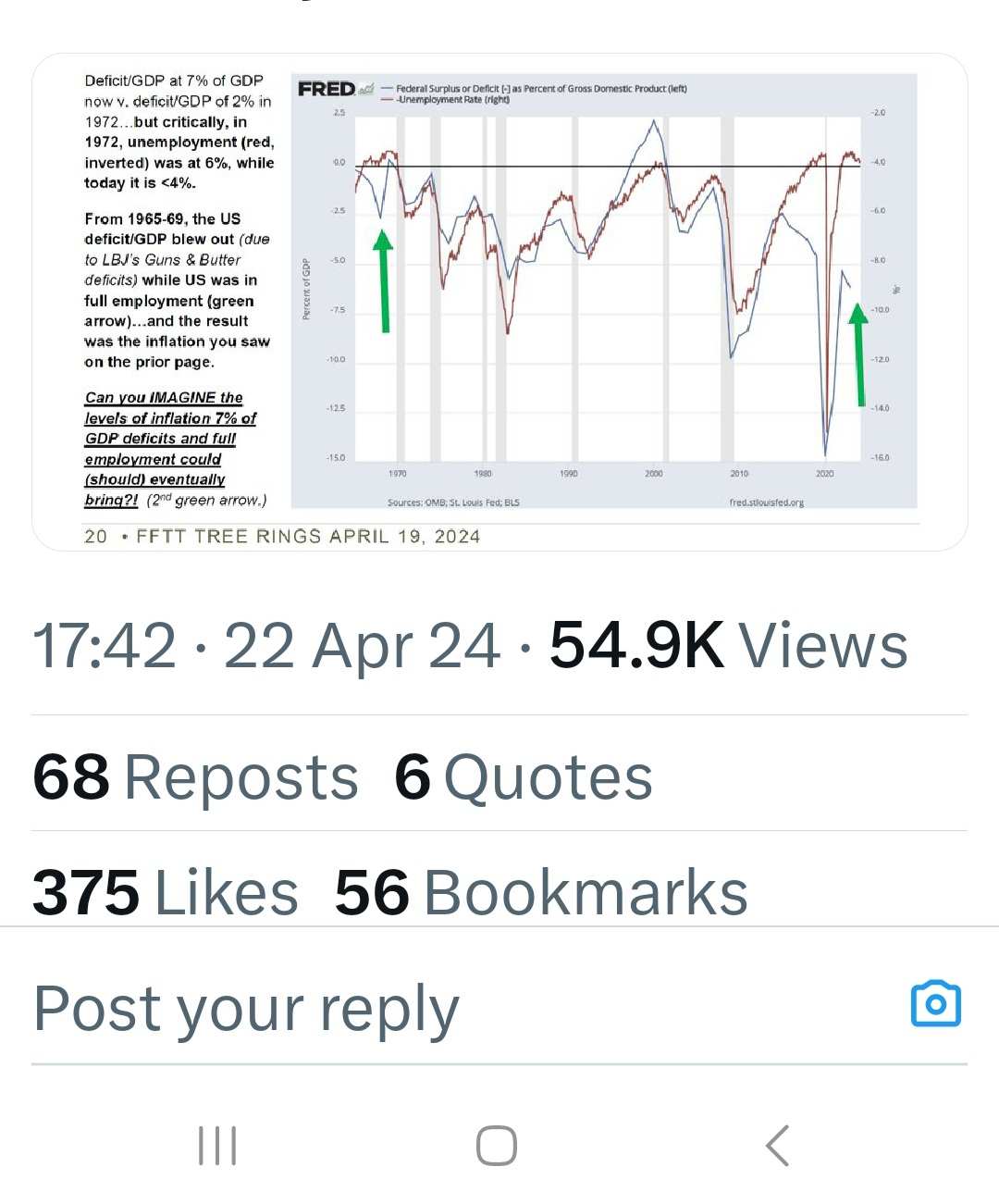

At least we know the break above US$2,050 in gold since February has them concerned enough to pull a margin increase at the COMEX right ahead of next week's FOMC meeting, and clearly shows that the FED is really stuck and out of bullets and gold knows it; 1. They are loosing money because long term rates are rising. 2. They have to raise rates do deal with inflation and long-term rates but would kill the stock market. 3. They have to lower rates to keep the stock market going, help real state, and ease the funding of all these wars. They are fully out of bullets and gold gets it, do you? Wake up and realize that for 4000 years gold has not been a Pet Rock but the vaccine for the consequences of Central Bank policy gone awry. -

Property crash, just maybe it really is different this time (Part 3)

HousePriceMania replied to spunko's topic in Property Prices & Economy

Who they going to sell to ? -

Credit deflation and the reflation cycle to come (part 9)

sancho panza replied to spunko's topic in Property Prices & Economy